Why Construction Loans Feel So Confusing

Most homeowners understand mortgages at a surface level, but construction loans operate under a completely different set of rules. Instead of financing a finished asset, lenders are funding a process with uncertainty around timelines, costs, and execution. That gap between expectation and reality is where most confusion begins.

Many homeowners only start learning how construction loans work after they have already chosen a builder, purchased land, or locked themselves into early decisions that limit their options. By that point, financing becomes reactive instead of strategic, especially for buyers still trying to decide whether it’s cheaper to build or buy a home in Texas.

Why Financing Decisions Shape the Entire Build

Financing is not a back-office detail. It directly affects what you can build, how much flexibility you have during construction, and how much risk you personally carry if something goes wrong. Loan structure influences everything from design decisions to how aggressively a builder can move.

Understanding the financing framework early allows homeowners to make decisions that reduce stress, prevent mid-build surprises, and keep long-term costs under control.

Perspective From the Lending Side

To explain how construction loans actually function in the real world, we spoke with Cole Vaughan, Vice President at Clear Fork Bank. His experience financing custom homes across North Texas and Possum Kingdom Lake provides insight into how banks evaluate risk, why certain projects get approved quickly, and why others stall or fail before construction even begins.

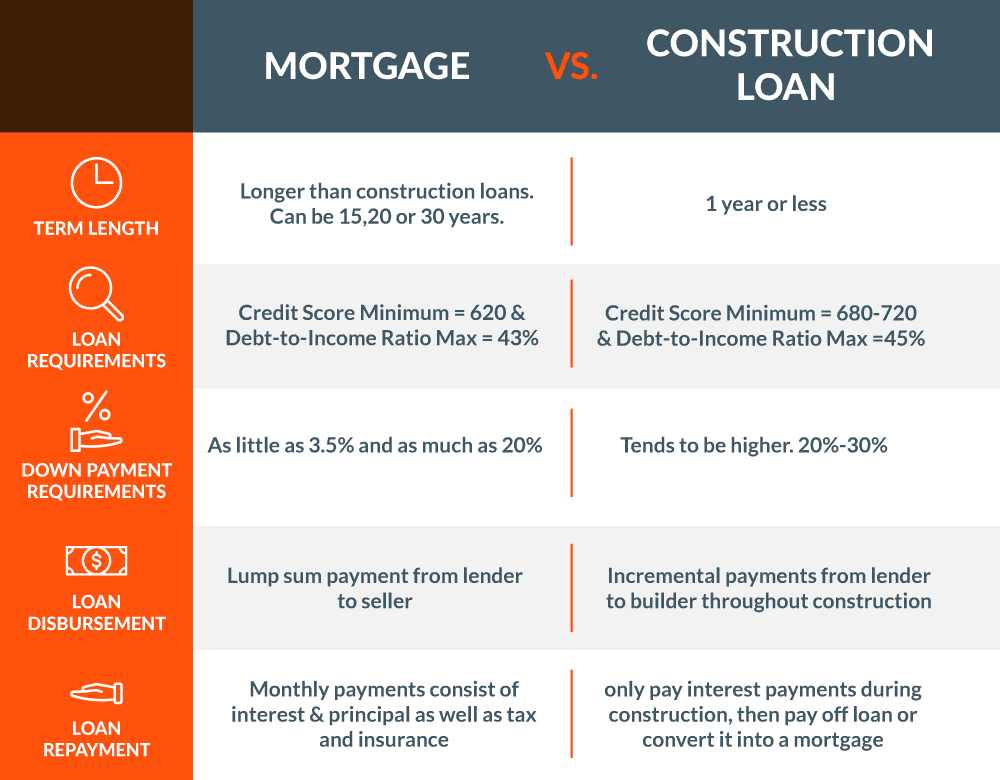

What a Construction Loan Is (vs a Traditional Mortgage)

Financing a Process vs Financing a Finished Home

A traditional mortgage assumes the home already exists, has a clear market value, and can be sold if the borrower defaults. A construction loan does not have that luxury. The lender is financing a home that will only exist months in the future, contingent on the builder executing the plan correctly and on budget.

Because of that uncertainty, construction loans are structured to limit exposure while the home is being built.

Interest-Only Payments During Construction

During the construction phase, borrowers typically make interest-only payments. These payments are based solely on the amount of money that has been drawn from the loan, not the full loan amount.

As construction progresses and additional funds are released, the outstanding balance increases, and so does the interest payment. This structure keeps payments lower early on while reflecting the real-time risk the lender is carrying.

Draw Schedules and Controlled Funding

Unlike a mortgage, construction loans do not release all funds upfront. Money is disbursed in stages, often monthly, based on completed work. These draw schedules are designed to ensure the home is being built as planned and that funds are not released ahead of progress.

This control protects both the lender and the homeowner from runaway costs or stalled projects.

Why Construction Loans Are Treated More Conservatively

Because the collateral is incomplete and illiquid during construction, lenders apply stricter underwriting standards. Income stability, builder credibility, budget realism, and location risk all carry more weight than they would in a standard mortgage scenario.

The Two Main Types of Construction Loans

Traditional Construction Loans (Two-Time Close)

How They Work

With a traditional construction loan, the borrower closes on a short-term loan used exclusively for construction. This loan typically has a 12-month window to complete the build and requires interest-only payments during that time.

Once construction is complete, the borrower must qualify again and close on a separate permanent mortgage.

Advantages

This structure often provides better long-term rate flexibility. Borrowers can shop for the best permanent mortgage once the home is finished and may benefit if rates decline during construction.

Tradeoffs

The main downside is uncertainty. Borrowers must requalify at the end of construction, which introduces risk if income changes, credit shifts, or lending standards tighten.

One-Time Close Construction Loans

How They Work

A one-time close combines the construction loan and the permanent mortgage into a single closing. Once construction is finished, the loan automatically converts into a long-term mortgage without requiring requalification.

Rate Structure and Adjustability

These loans are often adjustable-rate products with defined adjustment periods and caps. While they provide certainty around approval, they may expose borrowers to future rate changes.

Why Some Borrowers Prefer Them

One-time close loans appeal to borrowers with variable income, self-employment, or anticipated financial changes. Locking financing upfront removes the risk of failing to qualify later.

“The advantage of a one-time close is that if something changes in your financial outlook after construction – income, job structure, anything like that – you already have your mortgage in place. You’re not having to re-qualify at the end of the build.”

Choosing the Right Structure

The right loan type depends on income stability, risk tolerance, and expectations around interest rates. The decision is less about which option is objectively better and more about which aligns with the borrower’s financial reality and long-term plans.

The Construction Loan Timeline (Start to Finish)

Early Planning and Pre-Approval

Before any loan closes, lenders want to see a clear plan. That means preliminary drawings, a realistic budget, and a builder who can explain how the home will actually be built. At this stage, banks are pressure-testing assumptions rather than approving numbers. Weak planning here is the most common reason projects stall later.

Pre-approval focuses heavily on income stability and worst-case affordability, not optimistic projections. Lenders want to know the borrower can handle the loan even if rates rise or timelines stretch.

Closing on the Construction Note

Once plans and budgets align, the borrower closes on the construction loan. This is not a mortgage yet. It is a short-term note that exists only to fund the build. Equity requirements are applied here, and the appraisal is based on the home as if it were already completed according to the submitted plans.

Monthly Draws During Construction

Funds are released in stages as work is completed. Each draw corresponds to real progress on the site, not estimates or future work. This system keeps projects disciplined and prevents front-loading costs before value exists.

Borrowers pay interest only on the amount drawn, which means payments rise gradually as construction advances.

Completion and Transition to Permanent Financing

At the end of construction, the loan either converts into a permanent mortgage or is paid off and replaced with one, depending on the structure chosen. This moment is where preparation pays off. Clean execution during construction makes this transition smooth. Poor planning earlier makes it stressful and expensive.

How Banks Evaluate Construction Loan Risk

Cash Flow Under Worst-Case Scenarios

The primary question lenders ask is simple: can the borrower service this debt if everything goes wrong but the house still gets built. Banks stress-test payments using the highest possible rate and full taxes and insurance, not introductory numbers.

If cash flow fails here, the deal stops immediately.

Builder Credibility and Execution Risk

Banks are not only lending to homeowners. They are also betting that the builder can execute the project as planned. Experience with similar homes, reputation, and budget accuracy matter more than marketing or aesthetics.

This is why lenders prefer builders they know and trust. A great borrower paired with an unreliable builder is still a bad loan.

“The bank is just as much lending money to that builder as they are to the borrower. We’re assuming that builder can finish the house for what that budget says.”

Budget Realism and Finish Assumptions

One of the fastest ways to derail a loan is submitting a budget that assumes builder-grade finishes while planning high-end selections. Lenders see this mismatch constantly and adjust numbers upward when they know a market cannot support the proposed cost per square foot.

The closer the budget reflects reality, the smoother the loan process becomes.

Location, Market Familiarity, and Appraisal Risk

Appraisals capture market value, not build difficulty. Lenders rely on local knowledge to fill in the gaps. Homes in niche or lake markets are evaluated differently because resale risk, buyer pools, and construction challenges vary dramatically by location.

This is where local lenders often move faster and more confidently than large institutions.

Using Land as Equity and Other Financing Strategies

How Land Equity Is Actually Calculated

If a borrower already owns their land, that equity can count toward the required down payment. The bank orders an appraisal assuming the home is built on that land and credits the borrower for the land’s current value, not what they paid for it or what they hope it is worth.

Equity must still meet minimum thresholds, typically around 20 percent.

“We have an appraisal done as if the plans you submit are already built on that property. If you already own the lot and have equity in it, we can count that toward your down payment – but it still has to get you to that required equity position.”

When Land Helps and When It Doesn’t

Buying land early can be a strong strategy, but it rarely covers the entire equity requirement on higher-end homes. A low-cost lot paired with a high-cost build still requires additional cash.

Land equity reduces cash needs, but it does not eliminate them.

Pulling Equity From Other Properties

Some borrowers fund equity requirements by pulling cash from another owned property. This can work, but lenders factor the new debt into cash-flow calculations. What helps one side of the balance sheet can hurt the other.

Strategic Timing Matters

The most successful borrowers align land purchases, design decisions, and financing conversations early. Waiting until plans are finalized often removes flexibility and forces compromises that could have been avoided with better sequencing.

How Homeowners Typically Handle Housing During a Build

Carrying Two Homes vs Selling First

Some homeowners attempt to keep their existing home while building the new one. This only works when cash flow is strong enough to service both obligations simultaneously. In many cases, lenders see this as unnecessary risk, especially if the existing home has significant debt.

More commonly, homeowners sell first to simplify underwriting and reduce stress during construction.

Renting During Construction

Renting is one of the most lender-friendly strategies. It removes dual-housing risk and gives homeowners flexibility if construction timelines shift. Short-term leases or six to twelve month rentals are common, even if there is a penalty for breaking the lease early.

From a financing standpoint, this approach is clean and predictable.

Living On-Site or Temporary Setups

In rural and lake markets, some homeowners live in RVs or temporary housing on or near the build site. While unconventional, this can work when zoning and utilities allow it. Lenders focus less on where the borrower lives and more on whether expenses stay controlled and documented.

Market-Specific Norms Matter

What is normal in a metro area may be unusual in a lake or rural market. Lenders familiar with the area understand these differences and underwrite accordingly. This is another reason local knowledge matters.

The Most Common Financial Mistakes in Custom Home Builds

Taking on New Debt Mid-Process

One of the fastest ways to kill a construction loan is adding debt after pre-approval. New cars, large credit card balances, or financed purchases can push a borrower out of qualification even if the project is already underway.

Lenders often rerun credit before final approval or conversion to permanent financing.

Underestimating Finishes and Change Orders

Budgets often fail because early assumptions do not match final selections. Builder-grade pricing paired with high-end expectations creates a gap that has to be filled with cash later. Change orders compound this problem quickly and are one of the most common sources of cost overruns.

The more decisions made upfront, the fewer financial surprises during construction.

“Where people get in trouble is when the budget assumes builder-grade finishes, but what they really want is marble, quartz, or white oak. What they thought they could build for one price ends up being much higher once those selections start changing.”

Choosing Unrealistically Low Builder Budgets

Low bids are attractive, but lenders regularly see projects where the lowest number cannot support the finished home the borrower expects. Cost-plus contracts shift that risk back to the homeowner when reality sets in.

Banks often adjust budgets upward when they know a number does not match the market.

Lot-Related Costs That Don’t Show Up Early

Rock, dirt work, utility extensions, and site prep can dramatically increase costs, especially in elevated or view-oriented lots. Appraisals capture value, not difficulty. These expenses rarely appear until construction begins, which is why experienced builders and local realtors are critical early on.

Final Guidance for Homeowners Planning a Custom Build

Start With Builders, Not Lenders

Builders help define scope, cost, and feasibility. Lenders validate those assumptions. Starting in the wrong order limits options and creates rework later.

Compare Loan Structures, Not Just Rates

Construction loans differ more by structure than by headline rate. Understanding requalification risk, adjustability, and long-term exposure matters more than chasing the lowest initial number.

Use Local Experts Who Know the Market

Local builders, lenders, and realtors understand build costs, resale risk, and site challenges that outsiders often miss. That knowledge speeds approvals and prevents expensive surprises.

Plan Beyond Construction

Taxes, insurance, and long-term affordability matter just as much after the build is complete. The strongest projects are planned for the full lifecycle of ownership, not just the moment the keys are handed over.